Summary of Key Findings

1. Earned Wage Access is a preferred source of capital for users and is primarily used to manage regular household expenses

Across the four service providers, nearly all users are accessing a service like EWA for the first time, and it is the most preferred method of financing. Over the past six months, most users relied solely on EWA as a source for their credit or capital needs, with 87% of users from Ekko, 70% of users from KarmaLife, and 60% of users from Paywatch use it as their primary financial resource. Even among those who used additional sources of capital, EWA remained the preferred option across all service providers.

Our research indicates that 50% to 78% of EWA users depend on the service for regular household expenses such as groceries and utilities. Many users also utilize EWA for work-related costs, including transportation for wage earners or fuel expenses for gig workers.

2. Earned Wage Access improves users’ ability to handle emergencies

While the primary use-case for many users is to rely on EWA for daily expenses, it also serves as a resource to meet emergency expenses, with 15% to 39% of users in our studies reporting that they rely on it for urgent financial needs. 64% to 85% of users report an improved capacity to handle emergency expenses, with 17% to 44% experiencing significant improvements. These findings highlight EWA as a valuable part of employees’ financial toolkits.

3. Earned Wage Access enhances financial management, reduces stress, improves quality of life, and has a modest impact on savings

Across the four studies, 48% to 88% of users report improvements in their financial management, with 20% to 47% noting significant gains. Many users mention that the ability to meet expenses in the middle of the pay period helped them stay on top of their bills. Tighter financial management might have modestly helped users increase their savings, with 18% to 69% of users saying their savings have increased, with 4% to 18% noting significant gains.

This improved financial stability may explain why 29% to 85% of users report experiencing reduced financial stress, with 14% to 42% feeling significant relief. Notably, in Vietnam, female users were more likely than male users to report higher stress reduction, possibly due to their primary role in managing household expenses.

Overall, 63% to 96% of users across our studies reported an improved quality of life, with 16% to 36% citing significant improvements. Many users attributed these improvements to reduced stress, better financial management, and greater preparedness for emergencies.

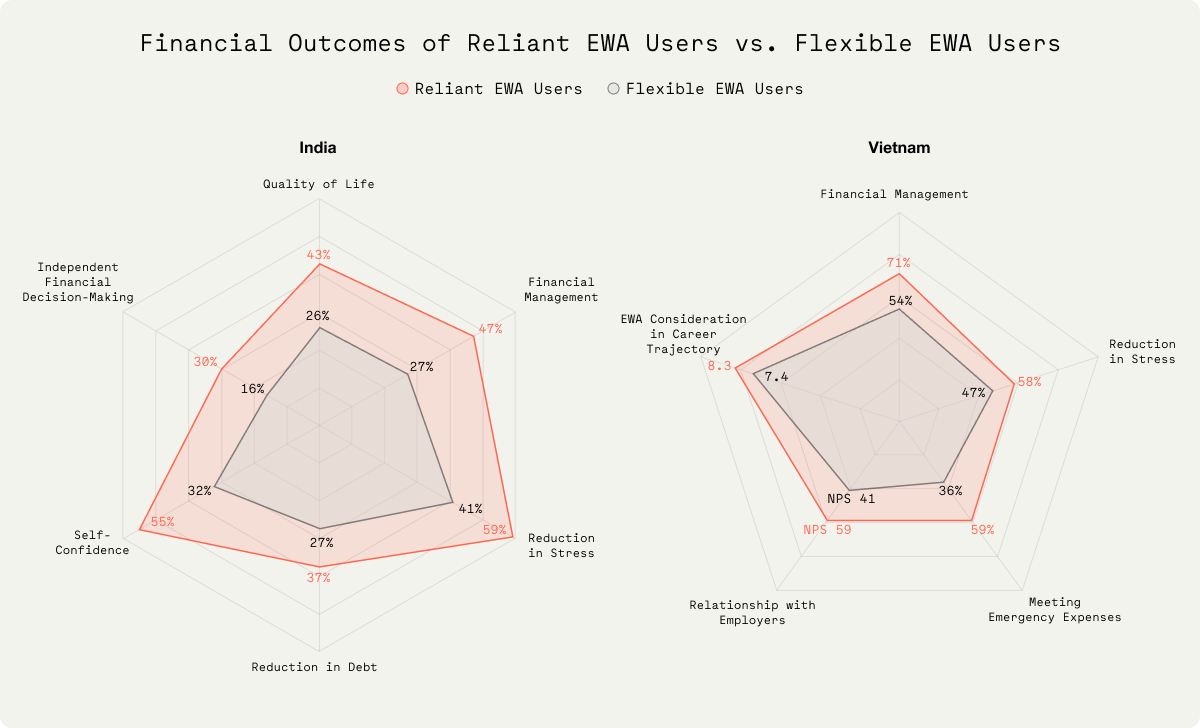

4. Regular EWA users report more substantial financial outcomes but also might be facing higher financial strain in meeting monthly expenses

Users who report that they rely on EWA with each pay period (‘reliant users’) report greater financial stability, lower stress, and improved emergency preparedness compared to users who rely on EWA as needed (‘flexible users’).

Reliant users – EWA users who report that they need to access EWA every pay period/month to meet their regular expenses.

Flexible users – EWA users who report that they do not need to access EWA every pay period/month to meet their regular expenses.

There is additional research needed to help asses EWA’s ability to be a strong financial planning tool in the long run. Data from KarmaLife shows that while reliant users saw a greater reduction in debt compared to their counterparts (37% vs. 27%) and saw improvements in their ability manage their finances (47% vs. 27%), they still found it difficult to cover monthly expenses (29% vs. 18%).

5. EWA is becoming an important factor in job selection

Many users consider EWA a crucial benefit when evaluating new employment opportunities. Employers who proactively offer such financial flexibility therefore might be better positioned to attract and retain top talent.

- In Paywatch, 46% of users rated access to EWA as “extremely important” in job selection, with an average rating of 8.6/10

- In KarmaLife, this sentiment is even stronger, with 70% giving it a 10/10 rating, with an average rating of 9.1/10

- In Ekko, 22% of users rated their need for EWA at the highest level, with an overall average of 7.9/10

- In SeamlessHR, 62% of users gave a 10/10 rating, with an average rating of 9.2/10

6. Users are highly satisfied with EWA and value the timely access to funds

Users from all four countries report high satisfaction with EWA, reflected in Net Promoter Scores (NPS) ranging from 51 to 60. The primary reason for this satisfaction is the timely access to funds.